Read and download the CBSE Class 12 Accountancy Dissolution of Partnership Firms VBQs. Designed for the 2026-27 academic year, these Value Based Questions (VBQs) are important for Class 12 Accountancy students to understand moral reasoning and life skills. Our expert teachers have created these chapter-wise resources to align with the latest CBSE, NCERT, and KVS examination patterns.

VBQ for Class 12 Accountancy Part 1 Chapter 4 Dissolution of Partnership Firm

For Class 12 students, Value Based Questions for Part 1 Chapter 4 Dissolution of Partnership Firm help to apply textbook concepts to real-world application. These competency-based questions with detailed answers help in scoring high marks in Class 12 while building a strong ethical foundation.

Part 1 Chapter 4 Dissolution of Partnership Firm Class 12 Accountancy VBQ Questions with Answers

VERY SHORT ANSWER QUESTIONS

Question. Which o the following will be Transferred to Realisation Account?

A. Goodwill appearing in the books at the time of Dissolution of Firm

B. Investment Fluctuation Reserve

C. Provision for Doubtful Debts

D. General Reserve

Choose the Correct Option:

1.D Only

2. A, B, C Only

3.Band C Only

4.Aand C Only

Answer. B

Question. In the event of dissolution of a partnership firm, the provision for doubtful debts is transferred to:

a) Realization account

b) Partner’s Capital Accounts

c) Cash account

d) Partner’s loan account

Answer. A

Question. On dissolution of a partnership firm, profit or loss on realization is distributed among the partners:

a) In capital ratio

b) In profit sharing ratio

c) Equally

d) None of the above

Answer. B

Question. Unrecorded liability, when paid on dissolution of a firm is debited to:

a) Profit & Loss account

b) Realizationaccount

c) Liabilities account

d) No need to record

Answer. B

Question. On dissolution of a firm, a partner paid Rs 700 for firm’s realization expenses. Which account will be debited?

a) Cash account

b) Realisation account

c) Capital account of the partner

d) Profit & Loss account.

Answer. B

Question. On dissolution of a firm, It’s Balance Sheet revealed total creditors Rs 50,000, total capital Rs 48,000, Cash balance Rs 3000, It’s assets were realized at 12% less. Loss on realization will be:

a) Rs 6000

b) Rs 11760

c) Rs 11400

d) Rs 3600

Answer. C

Question. An unrecorded asset was valued ar Rs 100000.On Firm’s dissolution, it was sold for 52%.Realisation Account will be credited with

a) Rs 48000

b) Rs 100000

c) Rs 52000

Answer. C

Question. A Partner took over the Investments of Rs 15000 at Rs 19000 on dissolution of a Firm. What amount will be credited in Realisation Account?

a) Rs 15000

b) Rs 19000

c) Rs 4000

d) Rs 23000

Answer. B

Question. Identify the sequence of application of assets at the time of Dissolution of a Firm:

A. Partner’s Loans and Advances

B. Partner’s Capital

C. Profit among the Partners at their profit sharing Ratio

D. Third Parties such as Creditors and Bank Loan

Choose the correct option:

1. D, C, B and A

2. A, B, C and D

3. D, B, C and A

4. D, A, B and C

Answer. D

Question. On Firm’s Dissolution, what entry will be Passed on realization of Goodwill which was shown in Balance sheet?

a) Goodwill A/C----Dr b) Cash A/C-----Dr c) Goodwill A/C---Dr

To Realisation To Realisation To Cash

Answer. Cash A/C----Dr

To Realisation

Question. Name the Asset that is not transferred to the Realisation account, but bring certain amount of cash against its disposal at the time of dissolution of the Firm?

Answer. Unrecorded Asset

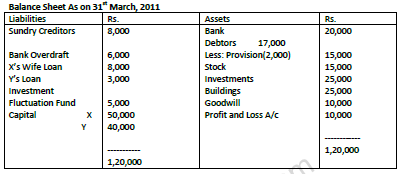

1. Following is the Balance Sheet of X and Y, who share profits and losses in the ratio of 4:1, as at 31st March, 2011:

The firm was dissolved on the above date and the following arrangements were decided upon:

(i) Y is authorized to sell the assets of the firm and will get a fixed amount of Rs.2,000 for his work.

(ii) X agreed to pay off his wife’s loan.

(iii) Debtors of Rs. 5,000 proved bad.

(iv) Y decided to sell the building for Rs. 9,000 to his brother. Market value of the building was Rs.80,000.

(v) Others assets realized _ Investments 20% less; and Goodwill at 60%.

(vi) One of the creditors for ,000 was paid only ,000.

(vii) Y took over part of Stock at ,000 being 20% less than the book value). Balance stock realized 50%.

(viii) Reali ation expenses amounted to ,000. State which value are being violated in the above question and also prepare Realization A/c.

1. Realisation A/c

• Values:

• Transparency

• Trust

• Mutual Understanding

Company Account – Issue of Shares

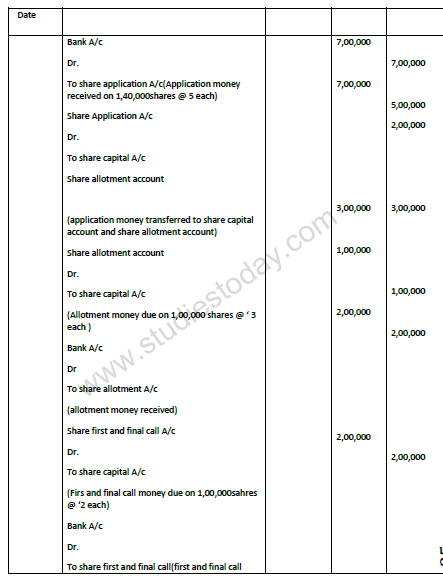

2. Shiksha India Ltd. Issues 1,00,000 shares of Rs.10 each payable Rs.5 on application, Rs.3 on allotment and Rs.2 on first and final call. Public applied for 1,40,000 shares and the company made the allotment to all the applicants on pro-rata basis.

Identify the value involved in the decision of company regarding allotment of shares.

Values involved

• Equality

• Responsibility towards investors

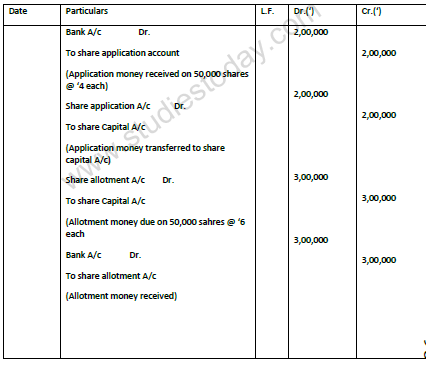

3. Rehan Ltd. Issue 50,000 shares of Rs.10 each payable Rs.4 on application and Rs.6 on allotment. According to the SEBI guidelines, a minimum of the net offer should be reserved for small investors. Therefore, out of these 50,000 shares, 50% portion is reserved for retail (small) investors. Issue has been fully subscribed . Identify the value involved.

3. Rehan Ltd Values Involved: Protecting the interest of small investors, Adherence to law

4. XYZ limited is offering 3,00,000 equity shares @ an issue price of Rs.50 when market price is Rs.100, to its employees as part of incentives. Nominal value of the share is Rs.10. What value/principle do you think that XYZ ltd is adopting towards its employees?

4. Values involved

• Employee Recognition

• Motivation

• Profit Sharing

• Satisfaction of esteem needs

5.Ramkay ltd. has a nominal capital of Rs.12 crores . Securities premium account shows a balance of `3 crores. The company does not want to carry the balance in securities premium account.

i. What are ways can the company make use of of the amount available in securities premium account?

ii. Suggest one best way of using securities premium account that will maximise the wealth of the share holders.

iii. Identify the value createdby the company by doing so?

5. Values involved

• Wealth maximization

• Responsibility towards shareholders

• Value addition

6.What do you mean by rights issue? What value do you think the company is trying to achieve by this type of issue?

6. Values involved

• Wealth maximization

• Continued patronage to the Company

7. Autumn ltd. is registered with capital of Rs.70 lakhs divided into equity share of Rs.100 each. The companyoffered for public subscription 1,00,000 shares of Rs.100 each. Issue was oversubscribed by 50,000 shares.The Company allotted the shares on pro-rata basis to all applicants.

a)What value/principle the company is trying to achieve by this method of allotment?

Just and Equitable

Motivation to existing shareholders

8.Vasanth& Co is a public ltd. company. It does not have its own articles of association. The company offered for public subscription of 10,000 shares of Rs.10 each. All money was duly received except for the call money of Rs.3 per share from Arun, holder of 100 shares, money. Though the company is deemed to have adopted TABLE A the company does not want to charge interest on calls in arrears.

Why in your view that the company does not want to collect interest on calls in arrears. What justification can the company give?

8. Sympathy

Generosity

Free study material for Accountancy

VBQs for Part 1 Chapter 4 Dissolution of Partnership Firm Class 12 Accountancy

Students can now access the Value-Based Questions (VBQs) for Part 1 Chapter 4 Dissolution of Partnership Firm as per the latest CBSE syllabus. These questions have been designed to help Class 12 students understand the moral and practical lessons of the chapter. You should practicing these solved answers to improve improve your analytical skills and get more marks in your Accountancy school exams.

Expert-Approved Part 1 Chapter 4 Dissolution of Partnership Firm Value-Based Questions & Answers

Our teachers have followed the NCERT book for Class 12 Accountancy to create these important solved questions. After solving the exercises given above, you should also refer to our NCERT solutions for Class 12 Accountancy and read the answers prepared by our teachers.

Improve your Accountancy Scores

Daily practice of these Class 12 Accountancy value-based problems will make your concepts better and to help you further we have provided more study materials for Part 1 Chapter 4 Dissolution of Partnership Firm on studiestoday.com. By learning these ethical and value driven topics you will easily get better marks and also also understand the real-life application of Accountancy.

FAQs

The latest collection of Value Based Questions for Class 12 Accountancy Part 1 Chapter 4 Dissolution of Partnership Firm is available for free on StudiesToday.com. These questions are as per 2026 academic session to help students develop analytical and ethical reasoning skills.

Yes, all our Accountancy VBQs for Part 1 Chapter 4 Dissolution of Partnership Firm come with detailed model answers which help students to integrate factual knowledge with value-based insights to get high marks.

VBQs are important as they test student's ability to relate Accountancy concepts to real-life situations. For Part 1 Chapter 4 Dissolution of Partnership Firm these questions are as per the latest competency-based education goals.

In the current CBSE pattern for Class 12 Accountancy, Part 1 Chapter 4 Dissolution of Partnership Firm Value Based or Case-Based questions typically carry 3 to 5 marks.

Yes, you can download Class 12 Accountancy Part 1 Chapter 4 Dissolution of Partnership Firm VBQs in a mobile-friendly PDF format for free.